Energy storage is an energy transition lynchpin encompassing countless technologies that vary on optimal context.

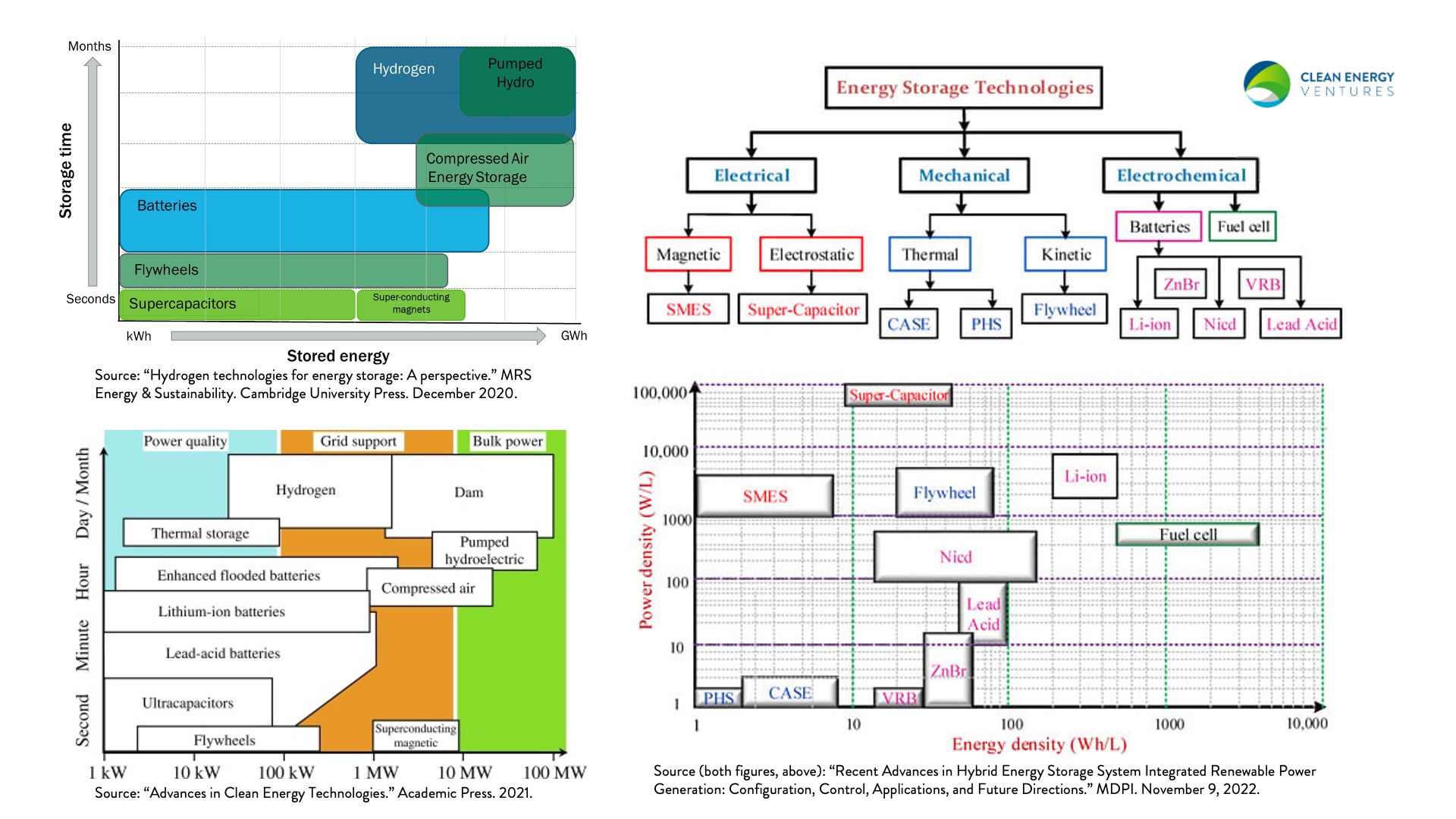

Literature typically landscapes energy storage as matrices or taxonomies on technical parameters. Figure 1, for example, captures recent such energy storage sector breakdowns.

As a climate tech venture capital firm that invests in companies with multi-gigaton-scale greenhouse gas (“GHG”) mitigation potential, Clean Energy Ventures’ (“CEV”) landscaping begins with evaluation on end use applications for which batteries are most needed for energy sector decarbonization.

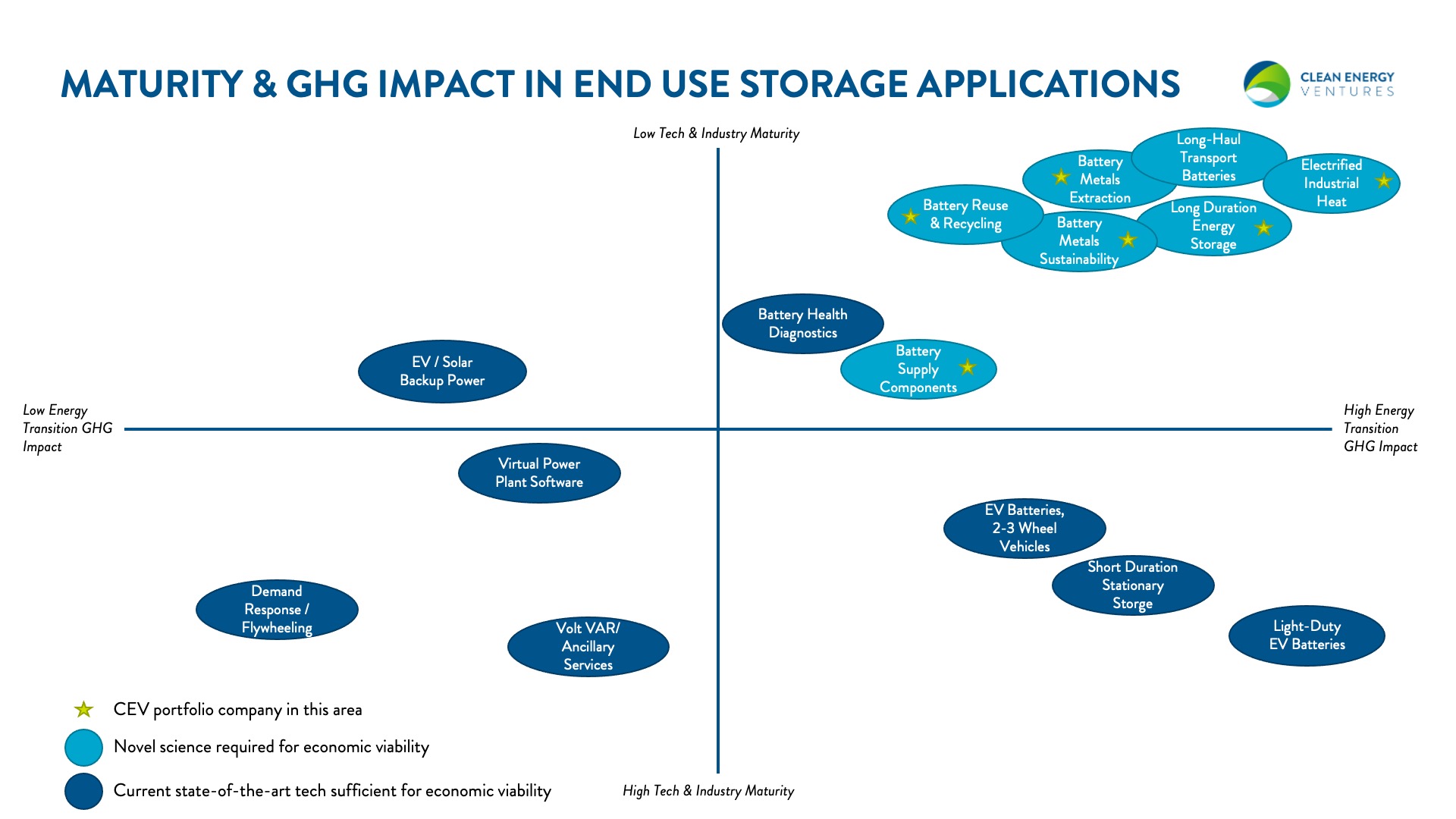

Accordingly, Figure 2, below, is a visual we developed late last year. It segments end use applications of batteries by GHG impact and industry maturity with a color coding for where breakthrough science is needed for economically viable solutions.

We believe startups solving the largest energy transition gaps have increased likelihood of becoming the largest companies, so we’ve targeted end use applications in the upper-right quadrant of Figure 2 for investment. Here’s why these upper-right applications are such critical energy transition gaps:

- Electrified Industrial Heat: Industrial heat accounts for 20% of global energy consumption and 10% of global CO2 emissions. Due to how difficult it is to decarbonize, International Energy Agency forecasts this sector potentially ballooning to 25% of global CO2 emissions by 2040. Solving for this challenge, CEV portfolio company Electrified Thermal has an electrified brick for storing solar and wind power and releasing it as industrial-grade heat at over 1,800oC temperatures. They’re enabling drop-in electrification of the hottest sectors like steel, cement, glass, ceramics, and others.

- Long Duration Energy Storage (“LDES”): Economic LDES is critical for pervasive grid decarbonization, so that intermittent renewables like wind and solar can function like baseload power. CEV portfolio company Noon Energy has invented a modular carbon-oxygen battery with a path to require only 10% the cost, 33% the mass and footprint, and 1-2% the rare earth elements relative to today’s state-of-the-art lithium-ion batteries when deployed in the 100-hour range.

- Long-Haul Transportation: Long-haul trucking and aviation are the two most difficult areas of the transportation sector to decarbonize due primarily to the need for energy dense fuels that perform in diverse climates and are amenable to quick refuel at costs competitive with fossil fuels. While “electrify everything” loyalists clamor for electric trucks and planes, CEV has not made such an investment. Batteries may not be the answer to this challenge. On the trucking side, we’ve invested in ClearFlame Engines, which has innovated an engine now powering long-haul trucks and gensets cost-effectively by burning alcohol-based fuels like ethanol and methanol instead of diesel with no performance sacrifice. For aviation, our current thesis is that methanol and sustainable aviation fuels are the lowest cost decarbonization pathways.

- Battery Metals Extraction: According to International Energy Agency (May, 2021), to achieve net zero energy sector GHG emissions by 2050, global production of lithium, graphite, cobalt, nickel, and rare earth minerals need to increase 42x, 25x, 21x, 19x, and 7x, respectively, by 2040 (see Figure 3, below). CEV portfolio company Nth Cycle has innovated a proprietary electro-extraction technology for processing battery-grade cobalt, nickel, manganese, copper, and other metals from both mine tailings and black mass from recycled batteries. CEV has also reviewed promising lithium extraction and refining technologies like Mangrove Lithium.

Figure 3 – Explosive growth in supply of key minerals are needed for the energy transition

- Battery Reuse & Recycling: Batteries are considered ‘clean’ due to their fit in a zero-carbon world, but their production and end-of-life require innovation to achieve this potential. Nth Cycle motivates battery owners to recycle batteries via improved extraction of valuable metals. Meanwhile, companies like Moment Energy are innovating affordable pathways of repurposing retired electric vehicle batteries.

- Battery Metals Sustainability: As with battery production, metals production currently struggles on sustainability in terms of impact on air and water quality, as well as GHG emissions. CEV portfolio company Travertine has invented a carbon capture method for mine sites that mineralizes captured CO2 via an additional, permanent removal method while producing sulfuric acid at the same time. Meanwhile, mining strategics like Rio Tinto co-invested with CEV on ClearFlame Engines to decarbonize gensets and trucking at mine sites.

- Battery Supply Components: Continued plummet of levelized cost of storage underscores the relative immaturity, and, thus, potential for innovation for lithium-ion and other battery chemistries. Cost is the limiting factor for pervasive storage assets, and innovations like Volexion’s conformal graphene coating for battery cathodes will drive battery costs down 25-30% by improving energy density 30% and cycle life 2x via a seamlessly drop-in approach supporting almost any battery chemistry.

Figure 2 is not comprehensive, and it evolves dynamically with new information. Companies frequently educate us on the extent of the GHG problem their technologies tackle, causing us to rework our landscape. We look forward to continuing to learn and adapt our perspective.

As the saying goes in venture capital, CEV has strong opinions, weakly held. We are entrenched in our commitment to decarbonizing the energy and industrial sectors at scale. And we look forward to growth from those who can improve our understanding of how best to achieve our mission.